Recent headlines surrounding tensions involving Iran and the broader Middle East have understandably raised questions from investors.

When geopolitical risks rise, markets can experience short-term volatility as participants assess possible economic impacts.

One area investors naturally watch is energy—particularly oil shipments through the Strait of Hormuz, a key route for global crude supply.

Energy markets often react quickly to uncertainty, but it’s important to remember that volatility does not always translate into lasting economic damage.

One structural difference in today’s environment is the position of the United States. Unlike past decades, the U.S. is now a net exporter of energy products,

including crude oil, refined fuels, and liquefied natural gas. That shift has strengthened domestic energy security and reduced the U.S. economy’s vulnerability

to overseas supply disruptions compared with earlier geopolitical crises.

Markets also tend to focus on the long-term incentives facing nations. Many countries across the region—including several Arab states—have increasingly

aligned around economic modernization, trade, and investment. Cooperation often delivers far greater prosperity than prolonged conflict. Historically, periods

of stabilization can produce what economists sometimes call a “peace dividend,” where reduced tensions allow capital, trade, and growth to accelerate.

For investors, the key takeaway is that while geopolitical events can be unsettling, long-term market direction is typically driven by economic

fundamentals—corporate earnings, productivity, innovation, and global growth.

We will continue monitoring developments closely and will update you if conditions change in a way that meaningfully alters the economic outlook.

As always, our focus remains on maintaining disciplined portfolios designed to navigate both calm and uncertain environments.

Please reach out anytime if you would like to discuss the current environment or your portfolio.

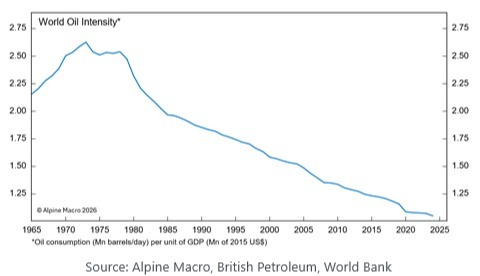

The World Is Much Less Dependent On Oil

The below chart shows that crude oil consumption relative to real Gross Domestic Product (GDP) is 60% lower today than in the 1970s and 34% lower than in 2000.

This is not to make light of the impact of crude on the world economy. Almost 60% of Asia’s oil supply comes from the Middle East, and therefore the passage through

the Strait of Hormuz is critical for the Asian economy. This is why Asian stock markets have fallen much more sharply than their American counterparts.

Meanwhile, gasoline prices remain a significant part of U.S. consumer spending, and crude prices have an important impact on overall inflation and, by extension,

monetary policy. By and large, high and rising oil and/or natural gas prices act like a tax hike for consumers, depressing their spending but propping up inflation.

While no one can know with certainty how the conflict or threats to energy infrastructure will unfold, the proximity of mid-term elections, the political importance of

affordability messaging, and coordinated strategic moves around energy security suggest the greater likelihood of a short-term price shock rather than a prolonged

disruption to global oil supply and shipments.

Investment Strategy: Keep It Simple

Rather than attempting to predict short-term market movements, we remain focused on several structural forces that may shape portfolio outcomes well beyond 2026.

First, investment opportunities should continue to broaden beyond a handful of mega-cap U.S. companies and dominant market themes. Many sectors across the

economy are positioned to benefit from advances in technology, productivity tools, and a potentially less burdensome regulatory environment.

Second, non-U.S. markets may benefit from rising infrastructure demand and ongoing economic reforms. Many businesses in friendly trading partner nations are

concentrated in industrial commodities and physical capacity—areas that may prove less susceptible to disruption from Artificial Intelligence than purely digital or

service-based profit models.

Finally, a sharp move higher in oil prices or the U.S. dollar could temporarily push bond yields higher. Should this occur alongside longer-term disinflationary trends

driven by technology and productivity gains, it could create an attractive entry point for fixed income—particularly if the next Federal Reserve cycle shifts toward rate

cuts in 2026 and 2027.

Markets will always face moments of uncertainty and surprise. History suggests, however, that disciplined investors who focus on long-term structural trends—rather

than short-term noise—are best positioned to compound capital over time. Our commitment remains the same: applying defined processes, thoughtful diversification,

and customized advice to help each client navigate an ever-changing investment landscape with confidence.